The Faces of Personal Finance Are Changing, and These Trailblazers Are Forging a More Inclusive Path

Last year, Aimy Steele discovered something she had never seen before in the world of personal finance advice: lessons that felt culturally relevant to her, and inclusive of her experiences.

Steele is no stranger to that world, and she’s extremely familiar with the financial gurus who have become the faces of paying down debt, budgeting and saving. She met Dave Ramsey after completing one of his programs and has avidly followed the teachings of David Bach and Suze Orman. But as a Black woman, Steele found that the advice from the traditional personal finance industry never felt truly relatable.

“We can't compare our stories and our oppressive experiences with that of our white counterparts, and then still say, ‘But I'm supposed to be doing the exact same thing they're doing,’” Steele says. “If I don't see someone who looks like me, then I don't explicitly link my fate to them.”

So Steele, 42, took matters into her own hands. She signed up for dfree, a faith-based personal finance program specifically designed for the Black community. Created in 2005 by DeForest B. Soaries, Jr. — a retired pastor of First Baptist Church of Lincoln Gardens in New Jersey — dfree walks participants through training courses and connects them with financial professionals. For three months, Steele logged into the program weekly from her dining room table, listening to facilitators discuss homeownership and debt elimination in the face of oppression. She felt much less alone.

And she isn’t alone. Many people of color have long felt left out of the traditional personal finance space. Experts say that much of the industry approaches advice as though all people are on equal footing. But systemic barriers have led the median wealth of white families to rise to about $184,000 while that number remains much lower for families of other or multiple races — at just around $23,000 for Black families and $38,000 for Hispanic families, the communities facing the biggest wealth gaps.

For years, dfree participants have been meeting up weekly in Black churches, sororities and community organizations across the country to learn about paying off debt, insurance and more, all while blending in conversations around racial inequality. Steele recently brought the program to her own church and became certified to facilitate the course. She says her dfree experience wasn’t only transformative because of the financial advice she took away, but also because the program acknowledged the discrimination Black Americans have faced for years.

“Hearing people talk about the fact that there is oppression validates what we have been feeling, thinking and knowing but could not articulate,” Steele says.

So do we throw all traditional personal finance advice out the window? Of course not. Countless people have changed their lives thanks to mainstream money tips. But making room for new faces, new products and new ideas in a world that has been so white-dominated for years is a necessary step — and it’s happening. There's a movement growing outside mainstream finance narratives that highlights control and empowerment, and it's being led by people of color, willing to reach an audience in whatever way they can. Getting there is the tricky part.

'Trauma can last generations'

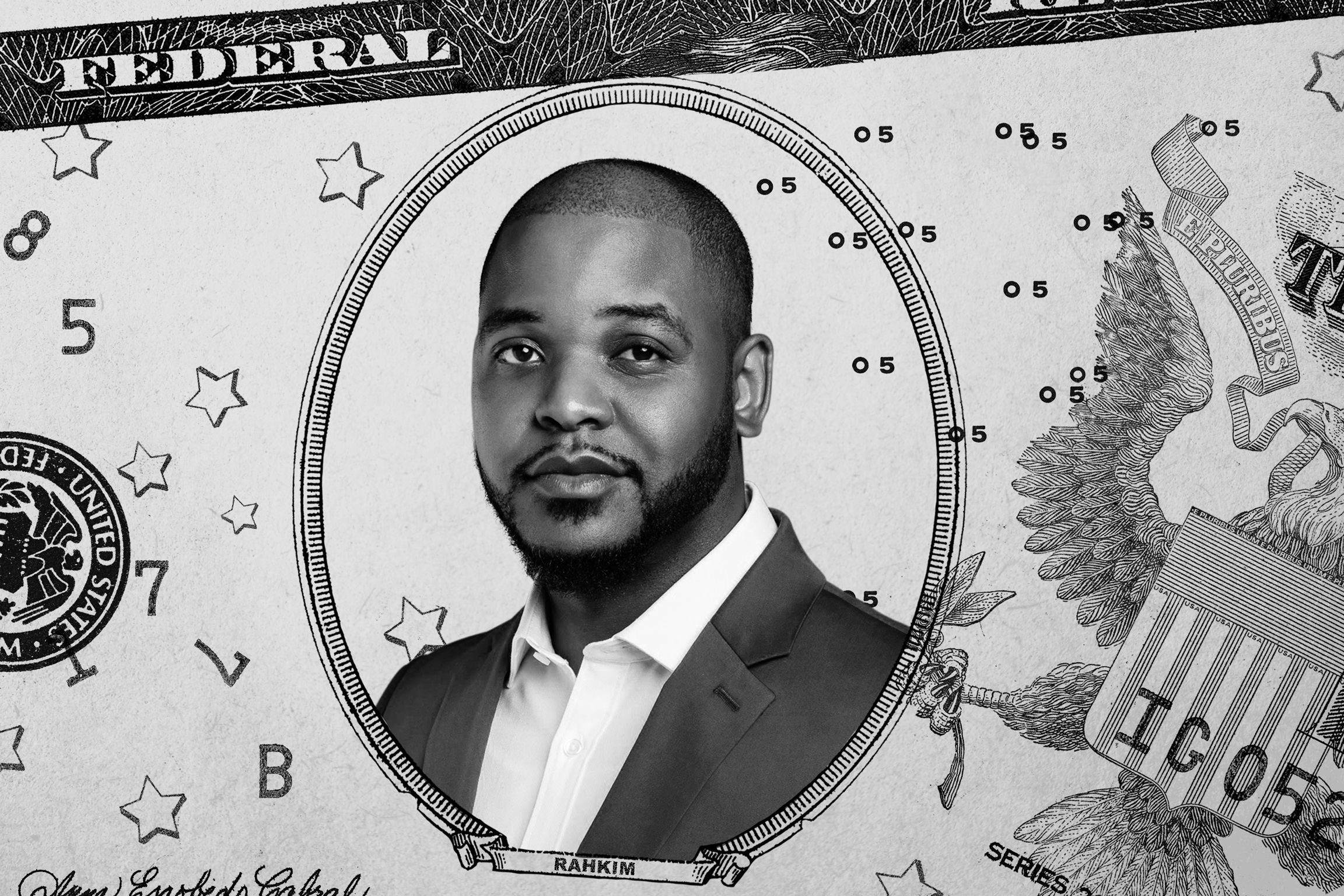

Rahkim Sabree distinctly remembers rushing home ahead of his siblings to tear an eviction notice off the front door before it was seen. There were times he couldn’t afford laundry, and food stamps didn’t always cover the groceries he loaded onto the conveyor belt.

“Situations like that are traumatic,” says the 31-year-old financial coach. “I never wanted to be poor again.”

As he grew up, he sought out as many sources as he could on building wealth, including Robert Kiyosaki’s well-known book “Rich Dad Poor Dad.” But he found that many of the financial texts he read didn’t acknowledge the financial trauma Black people have experienced in this country. That trauma, like the loss of $3 million after a bank created for emancipated slaves collapsed in the 1870s, reverberates throughout the community today, he says.

“When you work so hard to build up capital just to have it taken from you, that creates a trauma and that trauma can last generations,” Sabree says. “Grandma says don’t put your money into banks because they’re crooks, dad says don’t put your money in the banks because they’re crooks — and so you never put your money in the bank.”

Financial education for the Black community has to be unique to the Black community, says Sabree, who helps people work through their own financial trauma, which he says can range from an eviction or bankruptcy to having someone tell you credit cards will ruin your life. Part of the solution, he says, is to point Black people to Black-owned businesses and banks they can trust, like Greenwood, a mobile banking platform designed for Black and Latino customers that was co-founded by rapper Killer Mike. Greenwood provides monthly grants to Black and Latino-owned businesses and produces personal finance educational content targeted at these communities.

Distrust goes beyond banks and touches investing, insurance, credit cards and more, Sabree adds.

Racial inequality has seeped into nearly every aspect of our financial lives. At work, claims of racial discrimination are often the most filed claims but have the lowest percentage of success, and the wage gap shows no signs of shrinking. Meanwhile, Black borrowers are far more likely to be saddled with student loans than their white counterparts. One report found that 20 years after graduation, a typical white borrower has paid off 94% of their balance on average, while the typical Black borrower had paid off just 5%. When it comes to housing, our culture of homeownership was constructed on policies that led to discriminatory practices that still exist today, says Jacob Faber, an associate professor at New York University's Robert F. Wagner School of Public Service.

“We’re told almost from birth that the best way to build wealth is home ownership,” Faber says. “However, the opportunities to not only buy homes but also accumulate wealth through home ownership is deeply unequal.”

Real estate agents, for example, may steer home seekers to particular areas based on their race, and there’s a major racial gap in home appraisals. Last year, a white man and a Black woman shared that after replacing their photos with pictures of only white family members — and removing books by Black authors — their home appraisal jumped more than 40%.

“The reality of the lingering effects of discrimination and racism and their economic impacts are irrefutable,” says Soaries, the creator of dfree as well as New Jersey’s first male African-American Secretary of State. “The question now isn’t how this was formed, but what kind of strategies can be effective in helping people close the gap.”

New faces, new voices

The world of personal finance advice has always felt “not for me,” says Noemi Ibarra, a 24-year-old Latina woman based in Chicago.

Ibarra is a first-generation American, and her family has struggled with poverty ever since her parents immigrated to the U.S. from Mexico nearly 30 years ago. So when Ibarra graduated college and landed a full-time job, she was scared to invest her money.

“I didn’t know who to turn to,” Ibarra says. But then she found someone she could relate to: Giovanna Gonzalez, another first-generation Latina woman who has garnered more than 180,000 followers on TikTok with the account name “thefirstgenmentor.” Finding online mentors of color like Gonzalez has made Ibarra say she feels more confident that she, too, can build wealth.

Financial advice on social media has exploded over the last several years, for better or worse. The internet is especially popular for young people to get money advice, with 41% of Gen Z respondents to a 2021 Fidelity survey saying that they turn to social media influencers to educate themselves on investing.

Money experts of color are breaking into the online financial scene. The Budgetnista Tiffany Aliche runs a Facebook group of more than 480,000 members who are mostly Black women, which provides a natural starting place for members to relate to each other. Kiersten and Julien Saunders tackle “the deeply personal side of money through the lens of the Black American experience” via their Rich and Regular blog, podcast and YouTube series.

Delyanne Barros has more than 320,000 followers between Instagram and TikTok. The attorney launched her money coaching business just before the pandemic to share what she had learned about investing with everyone, especially other Latinos, she says.

These newcomers are much needed in the finance world. Gonzalez says she read over 50 personal finance books, but didn’t find that they address issues that hit close to her home, like planning for parents’ retirement and setting financial boundaries with families — concerns she says are specifically pervasive in Latinx communities, but families rarely talk about.

“Money is very taboo in our community,” Gonzalez says.

So she decided to do her part to help others, sharing videos with captions like “Struggling to set financial boundaries with your Latinx family? Try saying this” with advice from a licensed therapist. That particular video is a favorite of Anna Gamez’s, who says she struggles with this exact issue.

“Now I feel really comfortable going into conversations with family and friends,” Gamez, a 31-year-old job recruiter, says.

But not everyone does, or should, get their personal finance advice from social media. The financial advisor landscape needs to change as well, says Vaneesha Boney Dutra, an associate professor of finance at the University of Denver. Eighty-two percent of personal financial advisors are white, according to 2021 data from the Bureau of Labor Statistics. Because advisors looking for clients tend to start looking within their own circles, many of their clients also tend to be white, Dutra says.

“The industry is ignoring a very large piece of the population,” she adds.

The Onyx Advisor Network is trying to change that. Created by two financial advisors, Onyx is a network that focuses on helping “historically underrepresented advisors” start, scale and sustain their businesses by giving them tools, coaching and a network of advisors.

“We want to make sure that the industry looks a lot more like our country,” says Dasarte Yarnway, co-founder of Onyx, which announced its launch plans in December.

Yarnway didn’t even know financial advising was a career he could pursue until he landed his first job at a financial firm. He’s hoping that with platforms like Onyx, more financial advisors of color will see success, and in turn, help those who come after them to do the same.

Changing the financial world for future generations

Yemi Rose says he has always felt that traditional personal finance content does not speak to him.

“So many things default to white,” Rose says.

With his company OfColor — a financial wellness software platform that partners with employers and focuses specifically on helping employees of color — he hopes to help fill the gap. The platform connects employees with budgeting and savings tools, financial coaches of color and educational content geared towards non-white communities.

“People of color are not a monolith and there’s so much variation and nuance there,” Rose says. “But at the very least we try to attack what has been the traditional invisibility of people of color in personal finance.”

Beyond representation, there’s been a boom in financial tools and products specifically designed to help people of color better their finances. It’s an important change: the one-two punch of diverse racial representation in the personal finance space, as well as tools and products built specifically with these communities in mind.

Jean Smart can’t pinpoint exactly when she knew she had to leave her stable job at financial services giant UBS to start Penelope, which brings 401(k)s to small businesses, a majority of which are minority-owned.

“It was 1,000 cuts,” Smart says. They included seeing the disparities highlighted by the COVID-19 pandemic and the murder of George Floyd. Then, anti-Asian racist events came to light, and Smart says for the first time ever, she asked her mother not to leave her house for fear of her safety.

During that chaos, Smart, a Korean-American woman, found that clients she had helped during her 20-year career in the financial industry didn’t seem to need her help as much as other communities of color who were hurting. She quit her job and turned to those people instead, wanting to help them in the best way she knew how with a new team full of people of color and first- and second-generation immigrants.

So many retirement savings tools are difficult to understand — especially for a small business owner who is juggling tons of tasks at once. Penelope aims to bring them a more streamlined approach to saving for retirement with a 401(k) subscription model that cuts through the jargon, Smart says.

Smart is hopeful about the future. She named her company after someone who embodies why it’s so important to her to help make the financial industry more inclusive: her 10-year-old daughter Penelope.

“I think it’s going to get better,” Smart says. “I have to.”